The question we get most often from allocators considering their first managed futures allocation isn’t about strategy. It’s about structure: should I go through a managed account or a hedge fund?

It’s the right question. The strategy decision — trend following, multi-strategy, macro — is downstream of the structural one. The same CTA can run essentially the same program through either vehicle, and the experience of being a client looks very different depending on which you choose. Most of the operational risks, tax considerations, and ongoing-relationship questions are determined the moment you decide between an SMA and a pooled fund.

We’ve placed accounts at both structures for two decades, and we’ll say up front that we generally prefer separately managed accounts for the kinds of clients we work with — individuals, family offices, RIAs, and small institutions. But “generally” is doing a lot of work in that sentence. There are real situations where a hedge fund structure is the right answer, and we’ll walk through both sides.

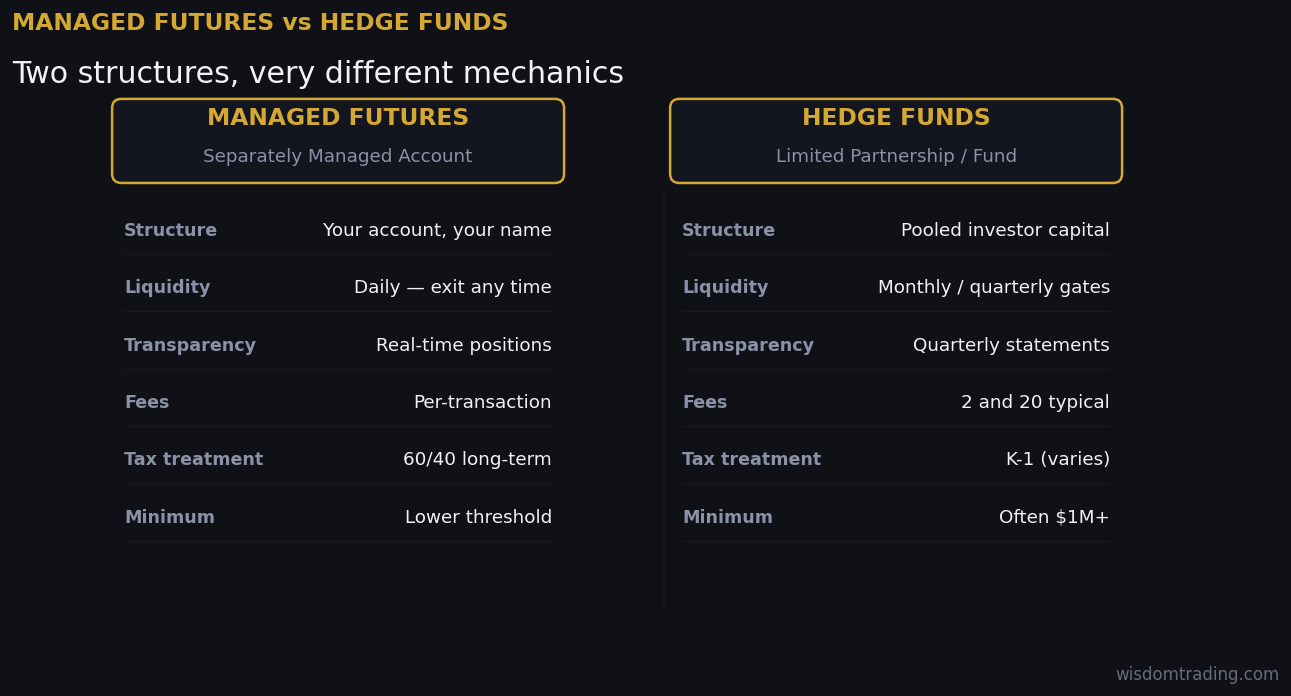

What each structure actually is

A managed futures account, more formally a separately managed account or SMA, is a futures account opened in your name at a futures commission merchant (FCM) — in our case StoneX Financial, Phillip Capital, or TradeStation. The commodity trading advisor (CTA) is granted limited trading authority over the account: they can place trades, but they can’t withdraw funds. Cash and positions live in your name throughout. You see them daily.

A commodity pool or hedge fund is a pooled investment vehicle — typically structured as a limited partnership or LLC — in which you own a share of the fund rather than the underlying assets. The fund’s manager (often the same CTA, sometimes a separate fund sponsor) holds the assets, makes the trades, and reports back to investors on a periodic basis. Your relationship with the underlying markets is mediated by the fund.

Many well-known CTAs operate both structures simultaneously. The same trend-following program might be available as an SMA with a $1 million minimum and as a fund with a $250,000 minimum. The strategy logic is identical. The investor experience is not.

Five practical differences that matter

1. Custody and control of assets

This is the headline difference, and it’s bigger than it sounds.

In an SMA, your cash sits in your account at the FCM under CFTC-regulated customer segregation. The CTA has trading authority but no ability to remove funds. If something goes wrong with the CTA — a key person leaves, the firm shuts down, the regulator steps in — you can revoke trading authority with a phone call and your account is intact.

In a hedge fund, the fund itself owns the trading account. You own a share of the fund. If something happens to the fund — gating, suspension of redemptions, operational failure — you become a creditor of the fund’s wind-down process, not the direct owner of the underlying assets. Most of the catastrophic outcomes in this asset class going back decades have been operational failures of pooled vehicles, not strategy failures.

None of this means hedge funds are dangerous. Most are well-run, audited, and operated by serious people. It means the assets are one structural layer further from you, and that layer matters when something unusual happens.

2. Liquidity and lockups

SMAs are generally very liquid. The positions are exchange-traded futures contracts, marked daily, closable during normal market hours. Capital can typically be added or withdrawn with a few business days’ notice, depending on the CTA’s notification requirements. There are no fund-level lockups.

Hedge funds operate on the fund’s terms. Many commodity pools allow monthly redemptions with 30 days’ notice. Some require quarterly redemptions. Newer or capacity-constrained funds may impose one-year lockups. Almost all reserve the right to gate redemptions if too many investors try to exit at once — a clause that rarely gets used but matters in stressed markets.

For an investor who treats managed futures as a strategic, long-term allocation, the difference may not matter day to day. For an investor who wants the option to rebalance, raise cash, or simply exit if the program stops working, the SMA structure is meaningfully more flexible.

3. Transparency

In an SMA, you see every position, every fill, every commission on a statement issued directly by the FCM — not by us, and not by the CTA. The statements are CFTC-prescribed in format. You can see whether the program is doing what the disclosure document says it’s doing, in real time.

In a hedge fund, you typically get a monthly net asset value, a periodic letter to investors, and an annual audited financial statement. You don’t see the trades. You don’t see the positions. You see what the manager chooses to disclose, mediated by what the auditor verifies once a year. Plenty of large hedge fund investors are perfectly comfortable with this — they’re paying for the manager’s discretion. But it’s a different relationship than the daily-transparency model of an SMA.

This matters most when you want to ask “is the program doing what I expected it to do during this kind of market?” In an SMA, you can just look. In a hedge fund, you’re inferring from monthly returns.

4. Fees

The headline fee structure is often similar — a management fee of 1% to 2% per year and a performance fee of 15% to 25% on new high-water-mark profits — but the details get interesting.

SMAs: you pay the CTA’s management and incentive fees directly out of the account, and you pay brokerage commissions per side at the account level. Everything is itemized on your FCM statement. There are no fund-level expenses on top.

Hedge funds: you pay the management and incentive fees, plus a layer of fund expenses — administrator, auditor, legal, regulatory, custody, sometimes a placement agent. These can add 30 to 100 basis points per year to total cost, depending on fund size. They’re disclosed in the offering documents but rarely advertised. Smaller funds carry proportionally more of these fixed costs.

For a $500,000 allocation, the difference can be meaningful — sometimes 50 to 100 basis points a year of structural drag in a fund vs an SMA running the same program. Over a long holding period, that compounds.

5. Tax treatment

In an SMA, you own the futures positions directly. Most U.S. futures contracts qualify for Section 1256 tax treatment: gains and losses are marked to market at year-end and taxed 60% long-term, 40% short-term — regardless of how long you held the position. For most U.S. taxpayers, this is a meaningful advantage relative to ordinary income rates on short-term gains.

In a hedge fund, you own shares of the fund. The fund passes through whatever its underlying activity generates — futures gains usually still qualify for 1256 treatment, but the math gets more complicated if the fund holds non-futures instruments, has Section 988 currency gains, or has UBTI considerations for IRA investors. K-1 reporting replaces the relatively simple 1099-B you get from an SMA.

None of this is tax advice and your situation may differ from someone else’s — talk to your CPA. But for taxable individual investors, the SMA structure is typically more tax-efficient and dramatically simpler to file.

When a hedge fund actually makes more sense

We won’t pretend SMAs are always the right answer. There are genuine reasons to choose a pooled structure:

Capacity-constrained programs. Some of the best CTAs only accept new capital through their fund vehicles because the operational overhead of managing many SMAs is prohibitive. If the program you want runs only as a fund, that’s that.

Below-minimum capital. SMA minimums for institutional-quality programs are often $500K to $1M and up. The same program through the manager’s feeder fund may accept $100K or $250K. For a smaller allocation to a flagship program, the fund is sometimes the only path in.

Strategies that span multiple instrument types. If the program trades futures plus OTC swaps plus equities, the SMA structure becomes operationally messy because you’d need multiple accounts at multiple institutions. A pooled fund holds all of it in one vehicle.

Investors who actively prefer one statement. Some allocators — especially family offices managing dozens of relationships — specifically value a single monthly K-1 and audited statement over the daily flow of FCM activity reports. The simplicity of the fund reporting is the feature, not the bug.

Non-U.S. investors. Offshore funds (typically Cayman or Bermuda structures) offer tax advantages and regulatory positioning that direct SMA ownership cannot. For most non-U.S. investors, the fund is the natural choice.

How to decide which is right for you

A few questions that tend to clarify the right structure:

How big is the allocation? Below $250,000 to one program, the fund minimums often force the answer. Above $500,000 to one program, the SMA option becomes available and the fee math usually favors it.

How important is liquidity? If you might want to exit on short notice — for rebalancing, capital needs, or simply because the program isn’t working — SMA. If you’re committed for a multi-year holding period, the difference matters less.

How important is transparency? If you want to see daily positions and explain to a board, family member, or yourself exactly what the manager did this month, SMA. If you’re comfortable with a monthly net return and an annual audit, the fund is fine.

What’s the tax situation? For taxable U.S. individuals with significant futures exposure, the SMA’s clean 1256 treatment is usually preferable. For tax-exempt or non-U.S. investors, the fund structure may be neutral or advantaged.

How much complexity can you absorb in your reporting? Multiple SMAs across multiple programs means multiple FCM statements, multiple disclosure documents, and a more involved year-end tax position. One fund means one K-1. For some investors, the simpler operations are worth the marginal fee.

How we work with both

Most of the managed futures programs we provide access to are available in SMA structure, which is what we’re typically recommending. We have working relationships with the major CTAs across the trend-following, multi-strategy, short-term systematic, and discretionary macro categories. When a client’s situation argues for a fund instead — allocation size, capacity, simplicity — we can route through the fund vehicle the same CTA offers. The strategy decision and the structure decision are separable, and we work both.

The principle that guides our recommendation in either case is the same: the client should be able to see, in writing, exactly what they own, exactly how every party in the chain is compensated, and exactly what the historical performance and risk profile of the program looks like before any capital is committed. That’s available equally in both structures. It’s just less work to verify in an SMA.

If you’re trying to decide

If you’re considering your first managed futures allocation, considering moving an existing allocation from one structure to another, or just trying to understand whether this asset class belongs in your portfolio at all — start the conversation. We’re a small firm by design and a principal who has been in the futures business since 2003 will respond, typically within one business day.

Past performance is not necessarily indicative of future results. Trading futures and options involves substantial risk of loss and is not suitable for all investors. The information on this page is for general educational purposes and does not constitute investment, tax, or legal advice or an offer to sell or solicitation to buy any specific investment product. Specific program details, including disclosure documents, are provided directly to qualified prospects under standard NFA-compliant procedures. Consult your own tax advisor about your particular situation.