When stock markets collapse, most investments bleed together. Bonds, stocks, hedge funds — all moving in lockstep downward. The one exception: managed futures strategies that follow systematic, trend-based trading rules.

The Problem with Traditional Diversification

For decades, the standard portfolio recipe was simple: 60% stocks, 40% bonds. When stocks fell, bonds were supposed to rise. In theory, you were protected.

Then came the credit crisis of 2008, the COVID crash of 2020, and the tech selloff of 2022. In all three cases, correlations spiked to 1.0. Stocks fell. Bonds fell. Everything fell. Investors discovered that “diversification” only works when the things you own don’t panic at the same time.

This is where systematic futures trading changed the picture.

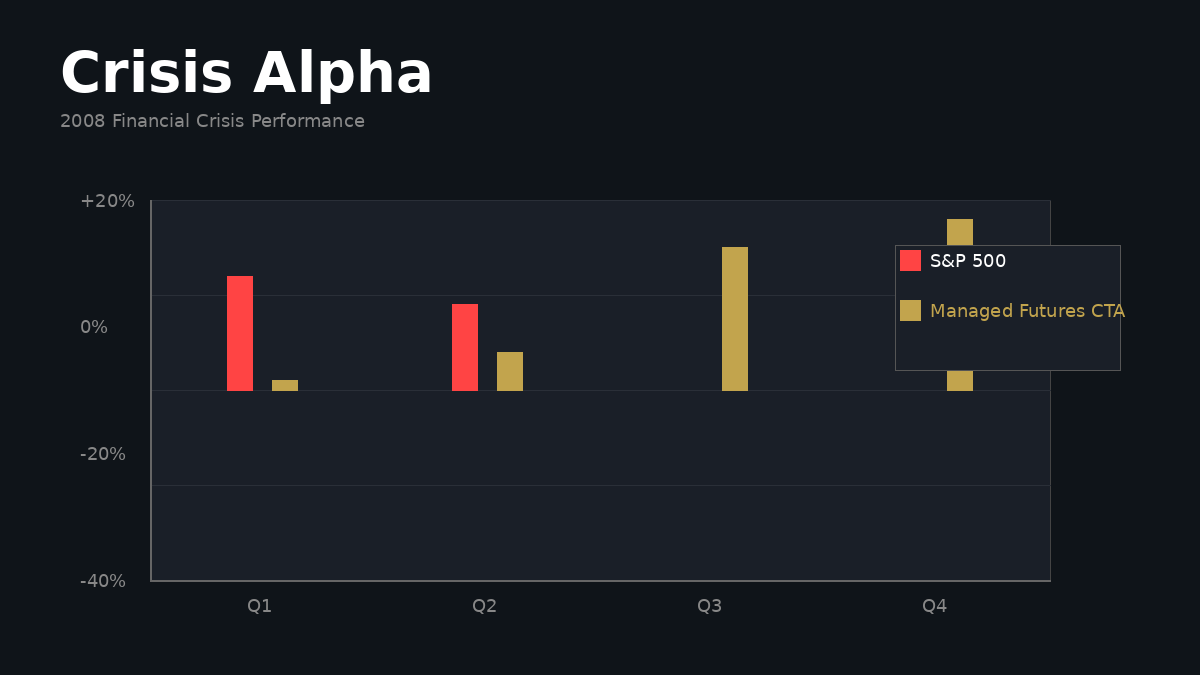

During the 2008 crisis, while the S&P 500 fell 37%, trend-following CTA indices returned +18% to +25%. During the March 2020 COVID crash, when equity volatility spiked 300%, systematic futures strategies again captured significant gains. This wasn’t luck. It was structure.

What Makes Futures Markets Different

To understand why, you need to understand how futures markets work — and how they differ from stock markets.

Futures are standardized contracts traded on regulated exchanges with a clearinghouse standing between every buyer and seller. The clearinghouse marks every contract to market daily, settling gains and losses. This means:

- Minimal counterparty risk. The clearinghouse is your counterparty, not some bank or hedge fund.

- Symmetric long/short access. Shorting a futures contract requires roughly the same margin (5–15%) as going long. No 150% short-sale restrictions.

- Extreme liquidity. Trillions trade daily across equity indices, rates, currencies, commodities, and energy. You can size in and out of positions without moving the market.

- Transparency. Every contract is identical. No opaque terms, no embedded leverage.

Compare that to traditional markets. When investors panic and need liquidity, futures markets remain orderly. When counterparty risk spikes, futures markets are insulated. When short selling becomes restricted (as it did in 2008), it’s never happened in futures.

This structural advantage is invisible during calm markets. It becomes decisive during crises.

Why Systematic Trend Following Works During Crises

A systematic trend-following strategy is simple in principle: identify direction, follow it, cut losses quickly.

During normal markets, this is a low-return, low-excitement strategy. Trends are choppy. Mean reversion is common. The risk-free rate on a Treasury bill is often a good baseline for performance outside of crisis periods.

During a crisis, everything changes.

What happens when equities crash:

- A massive group of long-biased investors (pension funds, mutual funds, hedge funds, individual investors) experiences sudden losses.

- Risk controls and leverage limits kick in automatically. Institutions are forced to sell.

- Correlations spike. Everything that was uncorrelated starts moving together.

- Liquidity evaporates in traditional markets (stocks, corporate bonds), but persists in futures.

- Massive persistent price trends emerge as waves of forced selling cascade across asset classes — not just equities, but currencies, interest rates, commodities, energy, metals.

A trend-following strategy, by design, doesn’t care which direction the trend is. It can profit from:

- Equities falling hard (short positions gain)

- Bond yields spiking (short rate positions gain)

- Currencies strengthening or weakening (long positions in moves)

- Commodities dislocating (energy and metals showing major trends)

The strategy is agnostic about why the trend exists. It profits from the fact that persistent trends exist — and during crises, they are most pronounced and most exploitable.

Performance During Crisis Periods

Historical data tells a clear story. Using data from major equity market crises (1998 LTCM crisis, 2000–2002 tech crash, 2008 financial crisis, 2020 COVID crash):

Crisis periods represent ~15% of trading days but account for 30–50% of systematic futures returns.

Outside crisis periods, managed futures indices typically return near the 3-month Treasury rate. This is exactly what you’d expect: in efficient, liquid futures markets with no systematic edge, you earn interest on your margin. Skilled managers may add a small risk premium from identifying dislocations, but it’s modest.

During crisis periods, the picture inverts. A strategy that earned 2% outside of crisis (in line with T-bills) can earn 8%, 10%, or 15% during a severe crisis month. It’s not dramatic daily returns—it’s the consistency of gains during the periods when everything else is breaking.

2008 Financial Crisis: S&P 500 vs. Trend-Following CTA Index

Crisis Alpha Isn’t Market Timing

Here’s a critical misconception: “Managed futures strategies are successful because they predict market crashes.”

This is wrong.

Systematic trend followers don’t predict crises. They react to them. And they don’t profit by being short everything — they profit by being positioned to benefit from the types of trends that emerge during crises.

During stable periods, trends tend to be choppy and mean-reverting. A strategy chasing trends will whipsaw. During crises, the signal-to-noise ratio improves. Trends are more genuine, more persistent, more exploitable.

The strategy doesn’t know a crisis is coming. It just adapts when market structure changes.

Crisis Alpha Decomposition: Where Do Returns Come From?

How to Think About Managed Futures in a Portfolio

If crisis alpha is your edge, here’s how to correctly size a managed futures allocation:

- It’s not a return driver during bull markets. Don’t buy a systematic futures strategy hoping it will outperform the S&P 500 during a 5-year bull run. It won’t. Treasury bills are often a better benchmark during calm periods.

- It’s an insurance policy with a positive expected return. Traditional tail-risk hedges (like out-of-the-money puts) have a known, negative cost. Systematic futures have a positive expected return in normal times and substantial gains in crises. That’s a free hedge.

- Size it based on your crisis tolerance. If you allocate 20% to managed futures and equities fall 30%, the portfolio draws 6% from equities but gains 3–5% from futures, netting around 3% loss. If you allocate 40% and the same crisis occurs, you might be nearly flat.

- Diversify across strategies. Short-term systematic, trend following, and momentum strategies all profit from crises but in different ways. A combination is more robust than a single approach.

Why Wisdom Trading Focuses on This

We’ve been building access to systematic trading strategies since 2003. We’ve lived through LTCM, the dot-com crash, the credit crisis, COVID, and the 2022 rate shock. In every major drawdown, the theme was consistent: allocators who understood crisis alpha preserved capital and bought opportunities while others capitulated.

The managers we recommend — whether they’re short-term systematic traders, trend followers, or momentum specialists — are built on this principle. They’re not designed to beat the market every year. They’re designed to be one of the few strategies that gains when traditional portfolios suffer most.

That’s the entire point.

2008 Crisis Performance by Asset Class

Conclusion

The financial markets of the 2020s are structurally more prone to crises than ever: higher leverage, faster capital flows, tighter integration, geopolitical fragmentation. If anything, the conditions that generate crisis alpha are becoming more common, not less.

Understanding how managed futures strategies profit from these moments—and how to position them in your portfolio—is the difference between a portfolio that diversifies in theory and one that actually does.

That’s what we help investors find. If you’d like to discuss how systematic futures strategies fit your situation, request details here.

Further Reading

- Kaminski, K., “Diversifying Risk with Crisis Alpha,” Futures Magazine, 2011

- Fung, W. & Hsieh, D., “The Risk in Hedge Fund Strategies: Theory and Evidence from Trend Followers,” Review of Financial Studies, 2001

- Lo, A., “The Adaptive Markets Hypothesis: Market Efficiency from an Evolutionary Perspective,” Journal of Portfolio Management, 2004